Data is the new oil: extraction of the infinity value

Banking and the Financial Services Industry is a domain where the volume of data generated and handled is enormous. Every activity of this industry makes a digital footprint backed by data. As the number of electronic records grows, financial services are actively using big data analytics to derive business insights, store data, and improve scalability. Technology has made the Banks to work in tandem to harness the data for intelligent decisions. This has prompted many organizations to disrupt their analytics landscapes and gather valuable insights from immense volumes of data assets stored in their legacy systems.

Big data consists of all data gathered by our electronic devices, both structured and unstructured, which can be processed with specific algorithms and analysis methods to manage and extract valuable pieces of information about the user. This data can be used afterward in various scopes, depending on the parties involved. In the FinTech sector, Big Data can be used to anticipate customer behavior, but also to create protective strategies and policies for alternative banks and financial institutions from all around the world. Each day, across the world, approximately 2.5 quintillion bytes of data are generated. And this rate is expected to grow furthermore shortly. Well, all this data can be used in multiple highly valuable ways, with the help of the appropriate tools and algorithms. Big data is crucial for personalized marketing, and with Big data, banks can continually track their customer behavior in real-time.

Following the Great Recession of 2008, which drastically affected global banks, big data analytics has otherwise enjoyed decade-old popularity in the financial sector. When banks began to digitize their operational processes, they needed to ensure different means which were feasible to analyze technologies like Hadoop and RDBMS (relational database management systems) for their business gains. These business gains have been made possible with the existing data analytics practices that have simplified the monitoring and evaluation of the vast amounts of customer data, which include personal and security information. With great trust in technology to handle the growing customer volumes and more transactions, the overall service level offered by the organizations has also enhanced. Working with Big Data, banks can now use a customer’s transactional information to continually track his/her behavior in real-time, providing the exact type of resources needed at any given moment. This real-time evaluation boosts the overall performance and profitability of the banking industry, thrusting it further into a growth cycle. Banking is an industry that generates data on each step, and industry experts believe that the amount of data generated each second will grow by 700% by 2020. The financial and banking data will be one of the cornerstones of this Big Data flood, and being able to process this data goldmine means gaining a competitive edge over the rest of the financial institutions.

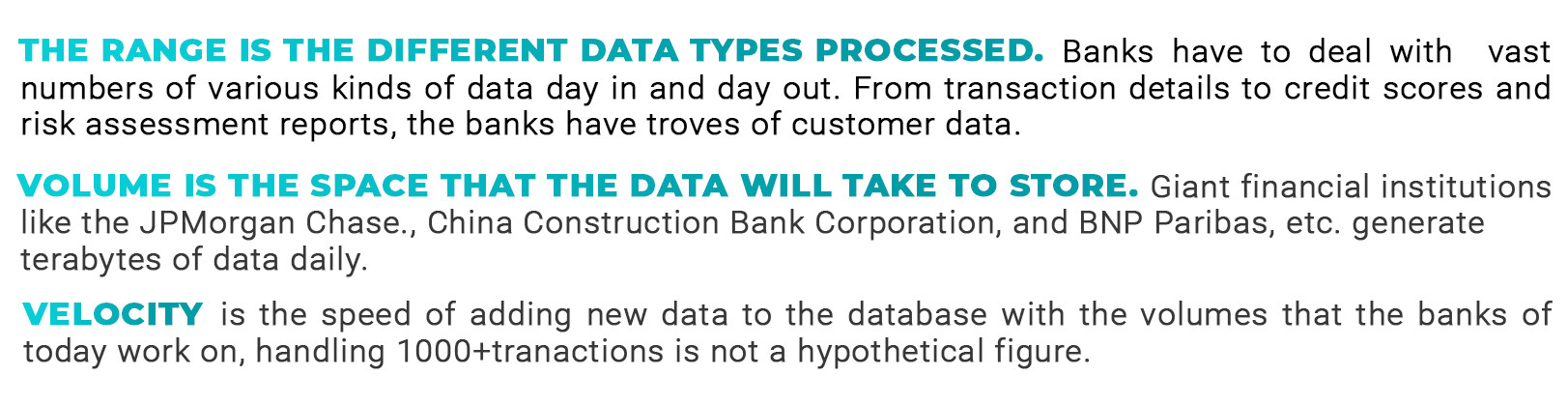

The big data can be described with 3 V’s. That includes variety, volume, and velocity. Here is how these relate to the banks:

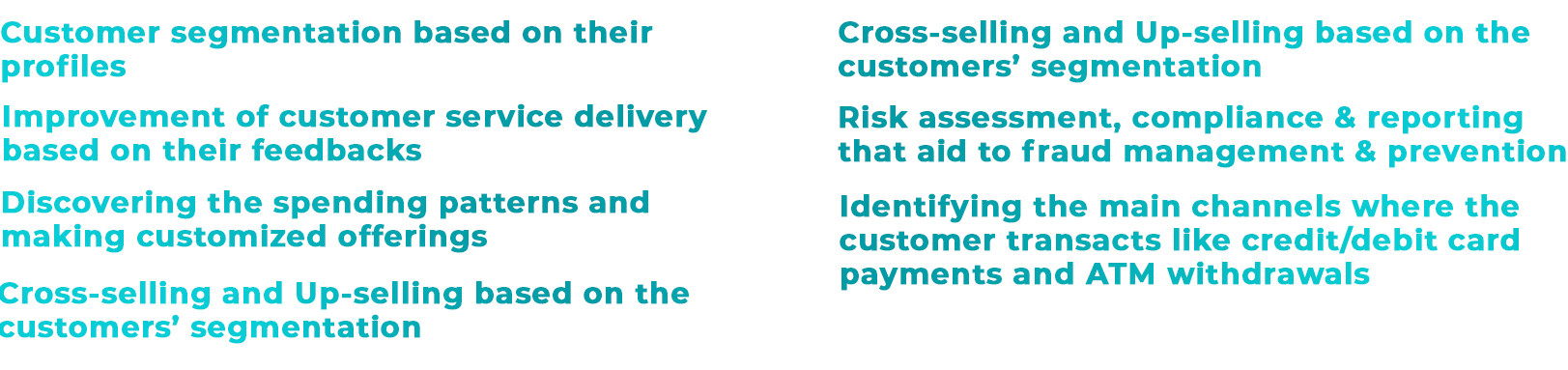

These 3 V’s are useless if a business does not have the 4’Th one, which corresponds to Value. The banks can make strategies based on these pointers:

Banks have several used cases to showcase the different ways where the data have been harnessed and used for intelligent analysis. This data opens up new and exciting opportunities for customer service by improving TAT and customized service offerings.

With so many financial institutions in the market, it gets tough for the customer to decide which bank to transact with. Customer experience, in this case, becomes a deciding factor. Big data analysis presents with the customized report for each customer, thus improving their services and offerings. FinTech companies are well-known for being customer-focused, and customer segmentation is one of their interest areas. The financial industry is focused on dividing their customers depending on age, gender, online behavior, economic status, and geographical coordinates. In this regard, FinTech companies can quickly analyze spending habits depending on age, gender, and social class. They can also easily tailor their services and alternate banking products to meet the demand and needs of each customer segment. The most valuable customers, namely those spending the most money, can also be identified. This will generate higher levels of customer satisfaction, as people generally seek highly personalized offers and financial products.

Big Data is used for customized marketing, targeting customers based on their spending. Analysis of customer behavior on social media through sentiment analysis helps banks create a credit risk assessment and offer customized products to the customer. In the banking and FinTech industry, like in many others, it is offering personalized services is one of the most excellent marketing tools available. Fintech companies like Contis Group claim that more and more customers have searched for personalized and flexible FinTech services and packages. The pressure to create customized services in the industry is also driven by the increasing number of companies that adopt such strategies, thus where a keen competition is present. Alternative banking institutions began to use the services of FinTech companies to improve their services and offer more personalized packages, but also a better, more comprehensive, faster infrastructure, which contributes to creating a more personalized and facile experience for the final consumer. Not only can FinTech companies identify spending patterns to make banking recommendations, but they can also use those to help the ultimate user save more money if this is one of their goals. Unlike traditional banking institutions, FinTech companies focus more on creating personalized financial services that meet the particular demands of the final consumer, and this is where Bid Data comes in the discussion.

Big data can be applied to bring immense value to the bank in the avenues of effective credit management, fraud management, operational risks assessment, and integrated risk management. Systems that enable with Big Data can detect fraud signals further analyze them real-time using machine learning, to accurately predict illegitimate users and transactions, thus raising a caution flag.

Another advantage of using Big Data in the financial industry is the fraud detection prospects that it opens. Obviously, with the rise of online banking and internet transactions, companies in the sector and their clients are more susceptible to fall victim to fraud. Big Data helps banks and other financial institutions to better understand the spending habits of each customer, but also their usual online patterns. In this case, when the enterprise detects unusual activity, the holder of the account can be easily contacted and ask or informed about a transaction that seems suspicious.

Risk management is an area of high interest in all industries. Once again, in the finance industry, Big Data comes with the immense advantage of identifying potential risks in terms of bad investments or bad payers. While Big Data cannot wholly prevent such risks, it can identify those at early stages and prevent further development into risky paths. Big data can help companies in the financial industry tailor programs and strategies that will assess the potential risks and minimize those.

The way we shop online will also be pushed forward by Big Data shortly. The combination of FinTech, social media and eCommerce data has the potential to develop significantly where and how we buy things online in the coming years. Twitter is at the forefront of providing a new channel for online purchases, but buying from your Twitter feed is potentially just the beginning. The data which can be gathered from Twitter’s new commerce system can teach the FinTech industry more about fast payment solutions and the demands which consumers and eCommerce firms have for more payment and banking options through a more comprehensive array of technologies connected to the internet of things. With more buying channels and a greater emphasis on customer experience, we are likely to see the FinTech industry help to bridge the gap between online and offline and help to create omnichannel systems for financial institutions and customer service in general. Big Data will allow FinTech firms to analyze customer needs better and make sure that they have access to the most appropriate payment technologies at the right time, have viable credit card limits, and have the most convenient processes for them at their disposal. The BFSI industry will obtain a better grasp of its needs, by aligning with the latest technologies like Big Data and the other global trends both internally into their operations and with customers. This will help the BFSI industry to provide improved services promptly with optimized operational costs. Though the implementation of Big Data on a large scale has just started to evolve in the BFSI industry, the sooner organizations adopt Big Data practices, the quicker they will be able to unlock the benefits this technology brings to their business.