Is Robo-Advisor a panacea of FinTech?

The success of FinTech upstarts has created an imperative for established financial institutions: embrace technology and customer experience innovation or risk losing business. A financial advisory has become one of the fastest facing sectors that are impending transformational change. Robo advisors have come to be a technology that has impacted the financial department in many different aspects through offering advice on investment, also minimizing both cost and conflict of interest. Through this, it has created assisted cost minimization and very accurate investment advice.

Before robo-advisors even became an option, there were only two options out there for most people, those two being managing your investments yourself, or hiring a financial advisor to help you. In our generation, today, there are a lot of younger investors compared to ever before since there are so many more resources out there for making investments. Currently, robo-advisors are being used by RIAs, and financial advisors, this is simply because rather than competing against the robo-advisors, companies have decided it would be better to work in parallel with them to allocate more strategy and create higher benefits. Overall, the best thing you can want as an advisor is efficiency. Another group of people that are using robo-advisors is the retirees since the growing number of baby boomers are coming towards retirement. This method of advisors has become very attractive towards them, specifically creating a bigger impact in terms of demographics in the generic financial advisor market, which is why robo-advisors should allocate most of their marketing resources to target this group of people. The main basis of the argument for robo-advisors is that, can computers start giving us financial advice on how we should allocate our money? The basis of a robo-advisor is to simply create an automated asset distribution method for investments through the use of algorithms. This is overall a good thing for the capitalist market that we currently have in the United States, moreover, whatever helps us get away from the high costs of financial advisors, there is a ton of positive competition in our market.

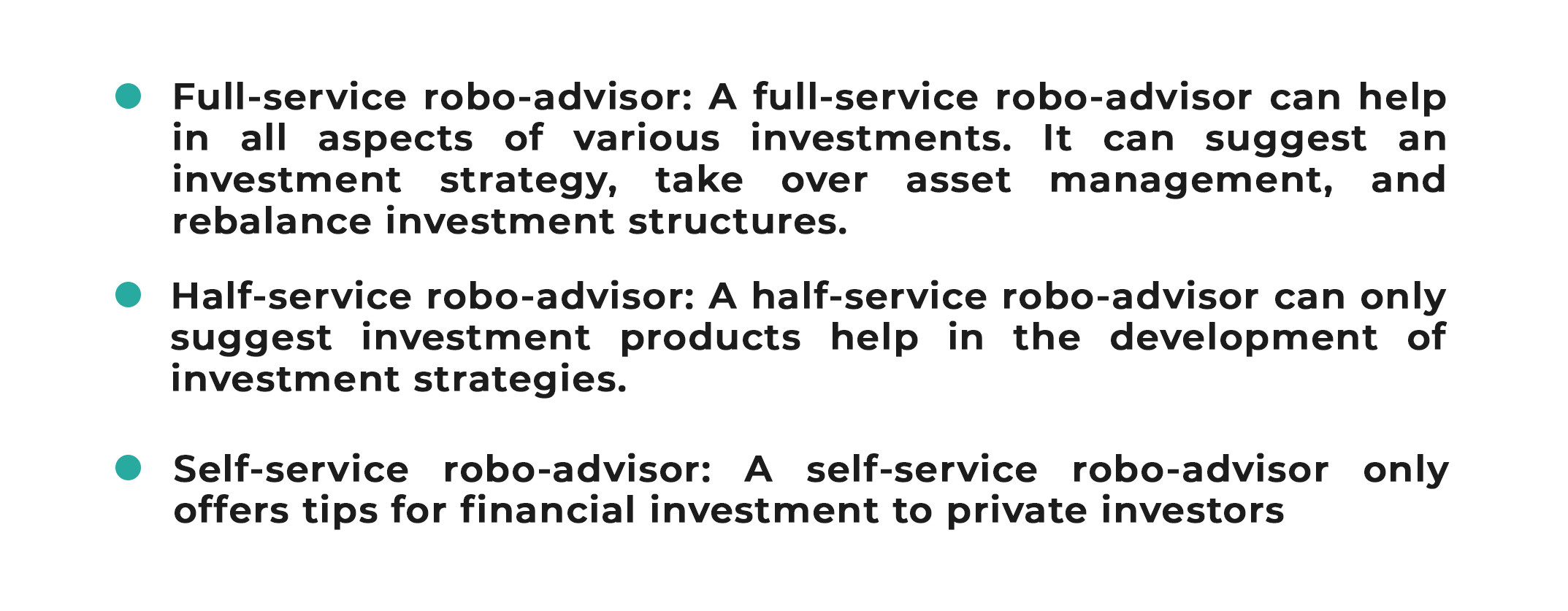

There has been a huge influx of robo-advisors into the market over recent years and while FinTechs were initially deploying the solutions, now many financial institutions have also developed their own. Most recently, Santander released its robo-advisor solution, entering the market late last year and aiming to separate itself from the competition by offering personal recommendations rather than just advice. Robo-advisors help private investors in wealth management with the help of predefined algorithms and trends in the financial market. The utilization of robo-advisors in FinTech is not a new phenomenon. Wealth managers have been using robo-advisors behind-the-scenes to gain additional information before offering their final recommendation to clients. As robo-advisors became more advanced, wealth managers were able to focus more on building client relationships and save time spent on data entry and investment management. Robo-advisors can be of three types:

The introduction of robo-advisors in FinTech can benefit investors and financial services in the following ways:

One of the primary functions of a robo-advisor in FinTech is automated customer onboarding. Robo-advisors collect vital data such as personal information, investment goals, and experience in wealth management through a detailed questionnaire. After obtaining all the required data, robo-advisors will analyze it using deep learning. Robo-advisors evaluate finances, risk tolerance, and investment strategies to maximize gains. Based on the accurate analysis, robo-advisors create customized portfolios. Robo-advisors offer critical wealth management advice and suggest investment strategies and services for customers.

Asset allocation is the process of selecting suitable investment strategies based on a user’s risk tolerance. Robo-advisors utilize predefined algorithms to determine the type of asset allocation. For instance, higher portfolio risk may be more suitable for investing in stocks whereas, lower portfolio risk may be suitable for investing in fixed income products. In this manner, robo-advisors in FinTech decide the most suitable asset allocation technique based on predefined models. Robo-advisors in FinTech can also help in rebalancing asset allocation. A customer’s specified percentage of investment in stocks and fixed incomes can change due to factors like reinvestment of dividends. Then, the customer may wish to rebalance their asset allocations. For instance, a user has an asset allocation with 40% fixed incomes and 60% stocks. However, their asset allocation changed to 30% fixed incomes and 70% stocks due to the reinvestment of dividends. In this scenario, the user may wish to rebalance to their original allocation structure to avoid risks. Robo-advisors can suggest techniques for rebalancing the asset allocation of their clients.

Robo-advisors in FinTech can estimate and predict how the portfolio balance of a customer would look like if the customer invests according to its strategies. For this purpose, robo-advisors analyze investment strategies and potential risks to understand their impact on personal finances in the future. Robo-advisors can make portfolio balance data more visually appealing by presenting a balanced curve based on mathematical function development or static growth. For example, a 60% investment in stocks and a 40% investment in fixed income may increase the portfolio balance by 3%. Alternatively, 40% investment in stocks and 60% investment in fixed income may increase the portfolio balance by 4%. With this approach, robo-advisors in FinTech can help users compare different investment strategies and determine the most suitable one. Hence, users can develop a data-driven approach towards wealth management with the help of robo-advisors.

Selecting the right investment policy and filing insurance claims can be extremely complicated. Generally, insurance policyholders may contact an insurance agent for insurance claims. Moreover, insurance claims processing requires multiple documents and the entire process can be time-consuming and tedious. The introduction of robo-advisors in FinTech can simplify insurance procedures right from selecting insurance policies to issuing insurance claims. Robo-advisors ask a series of questions to potential policyholders for gathering vital data. With the help of accumulated data, robo-advisors can suggest personalized insurance policies to the users. Additionally, in case a customer already has insurance coverage, then the robo-advisor can help to switch to a similar insurance policy and secure a refund, if possible. Robo-advisors can also accept insurance claims and process them autonomously. This approach of claims processing can be quicker than the traditional one. Some robo-advisors have managed to process and pay for claims within seconds.

In the state of South Carolina, individuals get a $50 tax deduction when they donate a dead deer to underprivileged people. Thanks to robo-advisors, people don’t need to move to South Carolina and hunt deer for tax deductions. Robo-advisors can help customers reduce the impact of taxes. As overall wealth increases, even small taxation rates can prove to have a magnified effect. Therefore, the right combination of investments from a tax perspective can be feasible in reducing taxes substantially. Robo-advisors can analyze personal income and the value of the estate to suggest suitable investment strategies. With this approach, the utilization of robo-advisors in FinTech can enable tax savings.

According to reports, 67% of Americans believe that they will outlive their retirement savings. Retire planning is a crucial aspect of wealth management that requires several documents for balancing taxes, managing income requirements, and estate protection. In the case of high net-worth individuals, the entire process of retirement planning can be complicated due to various business investments and assets. Hence, everyone needs a financial advisor for retirement planning. The advent of robo-investors in FinTech can simplify the process of retirement planning. Robo-investors can easily access each user’s portfolio to get an accurate estimate of their finances. Robo-advisors can analyze market trends to suggest an approach that would ensure maximum returns. Additionally, robo-advisors can help in the movements of securities to streamline the entire process.

Estate planning is a complex process involves preparing for probate, inheritance, disabilities, asset protection, and tax planning. For this process, estate owners have to evaluate the value of several assets that they own and decide the power of attorney. This process can be increasingly complicated for high net-worth individuals, who own multiple valuable assets such as artworks, properties, businesses, and luxury vehicles. Attorney’s and financial planner’s fees are another concern during estate planning. The adoption of robo-advisors in FinTech can streamline the entire estate planning process. Robo-advisors can access each user’s portfolio to evaluate the value of their estate. After accurate evaluation, robo-advisors can help in developing wills to simplify the procedure. Also, robo-advisors can suggest a suitable type of insurance based on the assets that a user owns. Robo-advisors can also help in asset protection and planning for disabilities and terminal illnesses. The adoption of modern technologies like AI, blockchain, and IoT has transformed various industry sectors such as retail, healthcare, production, and marketing. Similarly, modern technologies are evolving the world of finance. The adoption of AI-powered robo-advisors in FinTech will become a norm. Reports suggest that total assets worth $1 trillion will be managed by robo-advisors by 2020. Therefore, financial services must deploy robo-advisors to streamline various financial procedures.

The deployment of robo-advisors in FinTech will offer effective financial advice and automate asset management, investments, and insurance claims processing. Within this new technology, financial advisors offer investment management or financial advice online using less intervention since it is moreover based on algorithms. These new factors that are implemented in Robo-advisors are faced with the use of computer algorithms, by choosing appropriate investments mainly based upon time, and risk tolerance. Robo-advisors and their place in the future focus on the primal role it will play in our society. This class of advisors emerged as a body that is offering to fill the gap between human interaction, and so-called self-directed advisors. Robo-advisors are looked like the breakthrough in wealth management due to being able to bring services with low cost in comparison to current wealth management institutions. Being able to be given the client’s opportunities towards choosing active asset management, or passive allocation technique of assets have changed the game. Allocating client assets in numerous investment products such as real estate, stocks, bonds, funds, and retirement options. There are also various ways that clients will be able to use a mean-variance optimization method to fundamentally rational out how they look at their financials.